What AI Software Buyers Want From Pricing in 2026

TL;DR

AI gets priced one way and bought another. The market is moving toward usage, credits, and outcomes – more variable, harder to predict. Buyers are moving the other way: 68% rank a predictable total cost among their top three priorities when choosing an AI vendor, and just 19% rank the lowest entry price, the lowest-scoring factor tested. What wins the deal is pricing they can predict, understand, control, and defend internally – the four things "clarity" means to a buyer. The winning move is pricing a buyer can hold in their head.

Get the full buyer-preference data in our 2026 AI Pricing report

There's a disconnect in how AI software gets priced. Almost every pricing conversation starts from the seller's problem: AI costs are variable, so pricing should be variable too – move to usage, credits, or outcomes. The whole market is acting on that instinct.

But the seller's cost structure is only half the table. The other half – the one that decides whether a deal closes – is the buyer. Buyers reward pricing they can understand over even the most sophisticated variable model.

Pricing clarity breaks into four distinct requirements:

- Can I predict what this will cost?

- Can I understand how the pricing works?

- Can I control spending once we adopt it?

- Can I defend it internally?

Buyers consistently reward vendors that answer all four questions. Get them right and pricing becomes a reason to say yes. Get them wrong and even a fair price can stall a deal.

"Clarity" covers four specific things, each one measurable and each one a lever you can design for. (For how each pricing model works mechanically, our SaaS pricing models guide covers that in depth).

Clarity, part one: can the buyer predict the cost?

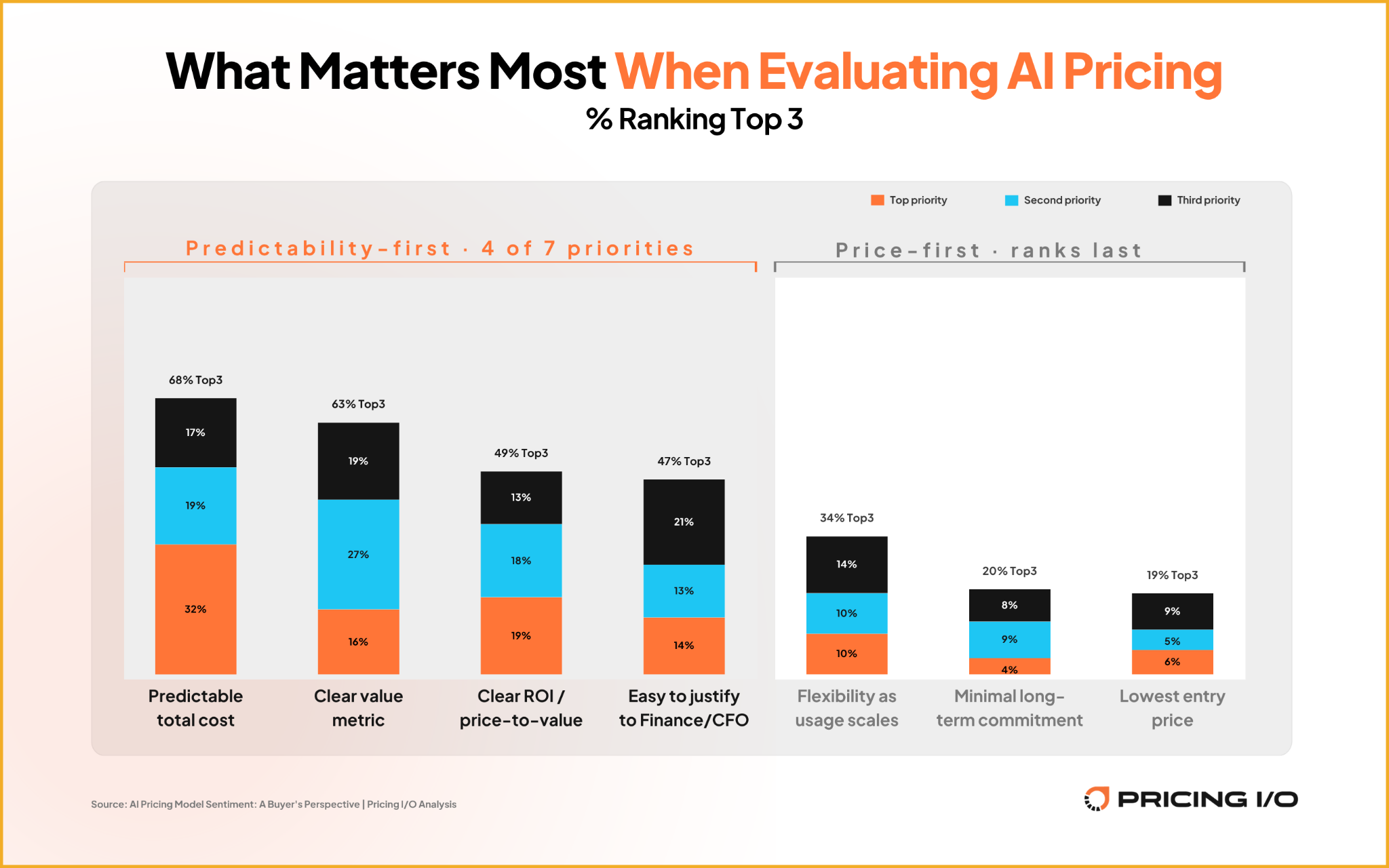

The first and largest component of clarity is cost certainty – and it outranks price by a wide margin. In Pricing I/O's 2026 survey of 296 software buyers, 68% rank predictable total cost among their top three priorities when evaluating an AI vendor; only 19% rank lowest entry price that highly, the lowest-ranked factor of any tested.

That ordering reframes what "good pricing" means to the person buying. Buyers shop for confidence about what the total will be, not the lowest sticker price – and they'll pay a premium to get it. That's why models with a fixed anchor consistently win and purely variable ones lose. Ranked by net preference (“the share of buyers naming each "most preferred" minus the share naming it "least preferred"), the models line up like this:

Every model in positive territory keeps a fixed anchor. The two buyers reject hardest are the pure variable models with no floor. Buyers will pay more as they use more; the objection is to losing the anchor that lets them predict the bill. This is the heart of the disconnect: the market is removing anchors in the name of aligning price to cost, and buyers consistently prefer models that retain those anchors. Lead with predictability, not a low headline number, and you're competing where buyers decide.

Clarity, part two: can the buyer understand how it works?

Predictability is about knowing the total. But knowing the total isn't enough. Buyers also need to understand how that total is generated. The second component is understanding how you get there, and buyers want both. After predictability, clearer pricing is the change buyers most often ask for in AI (35%), and a lack of usage transparency sits among their top concerns (61%).

Understanding breaks down when the pricing unit becomes abstract. Credit and token pricing is the hardest model to evaluate – 55% rate it harder to assess for AI than for traditional SaaS – because a "credit" means something different at every vendor, with no benchmark to translate into expected spend. Usage-based pricing is a milder version of the same problem; seat-based and fixed-anchor models are easiest, because the unit is something a buyer can already picture.

It changes what a stalled deal is telling you. One of the most common mistakes vendors make is treating uncertainty as price sensitivity. A buyer who hesitates on a usage or credit model is often not objecting to the price – they can't tell what the price will become. That's a design problem rather than a trust one, and it's fixable: a clear value metric, a way to estimate spend before signing, and visibility into consumption turn an opaque model into one a buyer can plan around. Much of what looks like a price objection is a forecasting problem.

Clarity, part three: can the buyer keep control of the spend?

Even a well-understood pricing model creates anxiety if spending feels uncontrollable. Understanding the model upfront isn't enough if the bill can run away after signing – so the third component is control. Buyers want assurance that adoption won't outrun the budget, and most are asking from experience: 89% of AI buyers have exceeded their initial budget. The cause is rarely the vendor – only about 10% blame a vendor changing pricing or terms after the sale. The usual driver is usage and adoption growing faster than anyone planned for, which makes this a forecasting and governance gap, not a question of vendor honesty.

The remedy buyers want is revealing: not a hard stop. They rank lowest the blunt controls – hard caps that halt the product mid-task, and prepaid credit pools that lock money up front. What they want most is visibility plus a decision point: soft caps that alert them and ask for approval before continuing (62%, the single most-wanted control) and predictive alerts before the budget is exceeded (55%). The product keeps working; the spend stays a choice. For vendors, that reframes guardrails from a nice-to-have into the cost of being trusted with consumption pricing – alerts, soft caps, and consumption visibility do more than limit usage; they give a buyer the confidence to scale.

Clarity, part four: can the buyer defend it internally?

The final component sellers often overlook is whether a buyer can defend your pricing after the sales conversation ends. Pricing decisions rarely rest with a single person. Most deals pass through finance, procurement, and often senior leadership before they are approved.

That makes the buyer evaluating your product only the first audience for your pricing model. At some point, they will have to explain it to people who were never in the room. The easier your pricing is to forecast, model in a spreadsheet, and justify in a budget review, the more likely it is to survive those conversations.

Many AI pricing models fail at exactly this stage. They make sense during a sales call but become difficult to defend when buyers need to estimate future spending and secure approval from finance or leadership.

"Easy to justify to finance" is a top-three priority for 47% of buyers, and it climbs as deals grow and more senior stakeholders weigh in. There's a structural reason it bites: IT is named the primary owner of AI cost risk by 67% of buyers, against just 17% for finance – so the person defending the spend internally is frequently not the one who controls the budget.

This is where the first three components of pricing clarity reinforce one another. Buyers can only defend prices they understand and predict. When pricing is transparent and spending is easy to forecast, champions can answer questions before they become objections. The easier you make it for a buyer to model your pricing and walk a CFO through the numbers, the further the deal is likely to travel.

Taken together, these four dimensions of clarity explain why some pricing models gain traction with buyers while others create friction.

What this means for how you price your AI product

Put the four components back together: buyers reward clarity, and clarity is something you can design. The market's race toward more variable pricing isn't wrong so much as incomplete – variability is fine, as long as the buyer can still predict, understand, control, and defend what they're signing. A few principles follow:

- Lead with predictability, not a low entry price. It's the priority buyers rank highest and the surest way to win their confidence.

- Anchor, then layer. Keep a predictable floor, then add a variable component that grows with the value you deliver – the structure behind value-based pricing buyers accept.

- Make the mechanism legible. Define your units clearly and give buyers a way to estimate spend before they sign. Thoughtful packaging makes this far easier.

- Build in control. Soft caps, predictive alerts, and consumption visibility let buyers scale without fear of a surprise bill.

- Design for the internal sell. Give your champion the numbers and the logic to defend the price when you're not there.

Do this and pricing stops being friction and becomes one of your strongest growth levers – easier to sell, easier to buy, easier to renew, and built to scale with the value you create. As AI pricing becomes more variable, the companies that preserve clarity will have an advantage over the companies that simply add complexity.

Go deeper with the buyer data

This piece covers what buyers want at the headline level. Our 2026 AI Pricing report breaks it down the way you'll want it when you're making the call for your product:

- How buyer priorities and model preferences shift by company size

- How budget ownership (IT versus Finance) changes tolerance for variable pricing

- Which models buyers find hardest to evaluate before signing, and what reduces that friction

- The conditions outcome-based pricing needs to work for buyers

- The usage controls and guardrails buyers value most, mapped to the concern each one resolves

Download the 2026 AI Pricing report (free)

Frequently asked questions

Is the lowest-priced AI tool usually the one buyers choose? No. Lowest entry price is the least important factor in Pricing I/O's 2026 AI Pricing report – a top-three priority for only 19% of buyers, versus 68% for predictable total cost. Buyers optimize for confidence in the total spend, not the smallest sticker price, and will often pay a premium for a model they can forecast.

Which AI pricing models are hardest for buyers to evaluate? Credit and token pricing is the hardest, because a credit can mean something different at every vendor and there's no familiar benchmark to forecast against. Usage-based pricing is a milder version of the same issue, while seat-based and fixed-anchor models are easiest to assess.

What usage controls do AI buyers want most? Soft caps with alerts and an approval step to continue (62%) and predictive alerts before the budget is exceeded (55%). Buyers rank hard cutoffs and pre-purchased credit pools lowest – they want visibility and a decision point, not a product that stops working.

Which AI pricing model do buyers prefer? Buyers most often prefer seat-based pricing, followed by subscription with fixed units. The common thread is a fixed anchor; purely variable models rank lowest. Buyers accept variability when it sits on top of a predictable base, which is why hybrid models do well.

Ready to grow with confident pricing?

Let's start a conversation with our team that will deliver practical value even if you don't work with us.

.png)

.png)