Credit-Based AI Pricing: Why Buyers Can't Forecast It – and How to Fix That

TL;DR

A credit means something different at every vendor: $0.005 at Salesforce, $0.25 at Lovable, a token at bolt.new, a "successfully run task" at monday. With no shared unit and no benchmark, buyers can't translate one vendor's credit into another's or estimate their own bill before signing – which is why 55% rank credit and token pricing the hardest model to evaluate for AI. The fix is design, not abandonment: define the credit consistently, anchor it, and make spend forecastable.

See the full credit comparison in our 2026 AI Pricing report

Credits and tokens have become the default way to price AI. They track the variable cost of running models, they stretch across a wide range of features, and they let a vendor charge heavy users more without forcing everyone onto the same plan. For a product team, the logic is sound.

For the buyer signing the contract, it's the model that creates the most doubt. In our research with software buyers, credit and token pricing was the hardest model to assess before committing – and the reason is specific and fixable. Above all else, what buyers want from AI pricing is a cost they can predict, and credits are where that breaks down most. This piece breaks down what a credit actually is across the market today, why that variation stops buyers from forecasting their spend, and what separates a credit model buyers trust from one they don't.

What is a credit, and what does it cost?

A credit is a unit a customer spends to perform an action in the product. That is where the agreement between vendors ends. Each one decides for itself what a credit represents, what it costs, and what spends it and the spread is enormous.

The clearest way to see this is to put the market side by side. Here is how ten well-known products define and price a credit today:

Three things move from row to row: the unit of measure (a token, an image, a task, a request), the cost per unit, and the definition of what triggers consumption. A credit at Salesforce costs half a cent; a credit at Lovable costs twenty-five – a 50x gap for the same word, attached to different work in each case. There is no exchange rate between them.

Why buyers can't forecast credit pricing

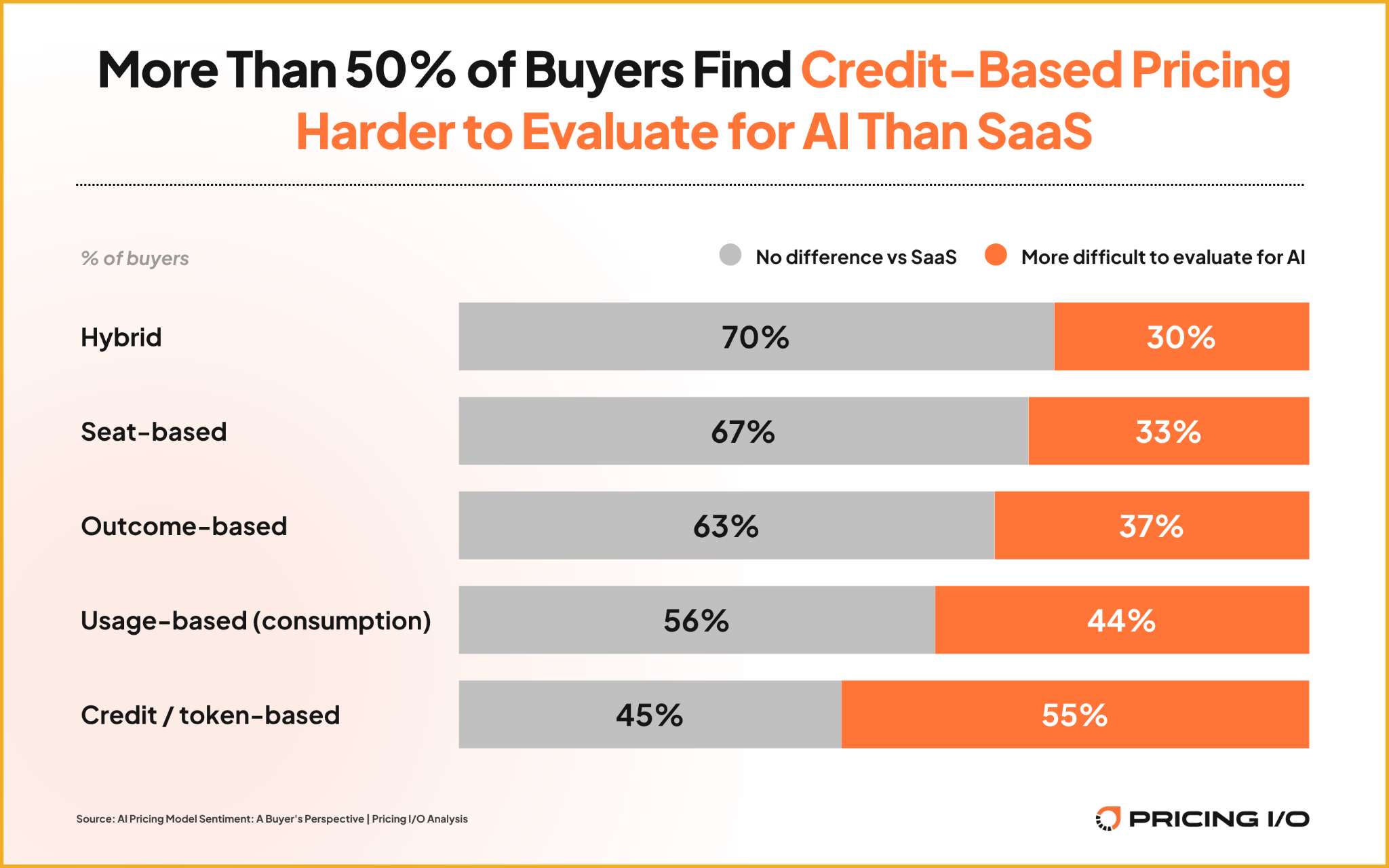

Because the unit is unstable, a buyer evaluating a credit model is asked to commit to a number they have no way to estimate. That is the heart of the problem, and it shows up in how buyers rate the model: credit and token pricing is the hardest of any model to evaluate for AI, named so by 55% of the 296 software buyers in Pricing I/O's 2026 survey. It doesn't ease up with scale either, holding between 54% and 59% from startups to enterprises – a sign the obstacle is the model itself, not a shortfall in any buyer's sophistication.

The most revealing detail is who struggles. You'd expect technical buyers to handle credits best; they handle them worst, finding the model harder to evaluate than non-technical buyers do (60% versus 48%) – the reverse of every model except seats. Even the people closest to how AI works can't forecast a credit, because the problem was never technical literacy. It's the absence of a benchmark. With seats, a buyer knows what they're paying for. With credits, there's no pre-AI reference point for what a credit costs or buys, which is why buyers rank it the model they're least confident evaluating before signing – a net confidence score of −11, against +29 for seat-based.

Sit in the buyer's chair for a moment. You can read that a credit costs $0.08. You still cannot answer the only question that matters – what will a normal month cost my team? – because you don't know how many credits your real work consumes, and a complex action might spend ten times what a simple one does. The price per credit is visible; the bill is not. Two buyers on the identical plan can pay wildly different amounts, and neither could have predicted it at signing.

This is why credit pricing produces more friction than the models around it, and the friction is worth diagnosing correctly. Vendors read it as a price objection and respond with a discount. The real issue is that the buyer cannot model the cost at all – the same root cause behind pricing guesswork that stalls deals. A buyer who can't forecast doesn't negotiate; they delay, and most never say why.

Some say it plainly. One buyer in our research put it this way: "We're unlikely to adopt new AI features if there is a credit/usage cap or upcharge associated with them. We're actively avoiding AI features that have this pricing mechanism." That is the cost of an unforecastable model stated out loud – not a demand for a lower price, but a decision to walk.

What separates a credit model buyers trust from one they don't

The encouraging part is that none of this is inherent to credits. The difficulty comes from how the model is built, and the difference between a credit system buyers can plan around and one they avoid comes down to a handful of design choices.

A credit model earns trust when:

- The definition is consistent. Sales, finance, and product all describe a credit the same way. Ask three people what one is worth and you get one answer.

- Buyers can forecast their needs. A customer can estimate usage before they commit, rather than guessing and then either hoarding unused credits or blowing through them.

- One credit maps to one discrete, measurable action. The unit means something a buyer can count, not an internal abstraction.

- Allotments are intentional. Heavier users pay more because they get more, and the logic is legible.

- Rollover and expiration rules are documented and enforced consistently – and don't change without warning.

A credit model loses buyers when those flip: the worth of a credit depends on who you ask, costs swing from five credits to fifty for similar-feeling actions, per-user and per-team allotments blur together, and the rules shift after signing. Each of those takes away the buyer's ability to forecast, and forecastability is the whole game.

The practical move for most products is to stop letting the bill float entirely. Pair credits with a predictable base, tie the credit to an action a buyer recognizes, and give them a way to estimate spend before they sign – a calculator, or a benchmark drawn from a comparable customer segment. Add alerts and soft caps so a busy month can't surprise them. One thing buyers don't want as the answer: pre-purchased credit pools, which rank near the bottom of the controls they'd choose – locking money up front doesn't solve the forecasting problem, it just moves it earlier. Done well, a credit model becomes a clean way to charge for value as customers grow – the aim of value-based pricing done well – rather than the thing that costs you the deal.

Go deeper with the buyer data

This piece covers why credit pricing is hard to evaluate and how to build one that isn't. Our 2026 AI Pricing report goes further:

- The full vendor-by-vendor credit comparison, with cost structures and definitions

- How evaluation difficulty breaks down by company size, industry, and seniority

- The complete good-versus-bad credit model checklist

- How credit and token pricing compares to seat, usage, and outcome models on buyer preference

Download the 2026 AI Pricing report (free).

Working through a credit or consumption model and want a second set of eyes before it ships? Book a call – we help B2B SaaS teams get AI pricing right.

Frequently asked questions

What is credit-based AI pricing? A model where a customer spends credits (or tokens) to perform actions in a product, with different actions costing different amounts. It's flexible and tracks variable AI costs well, but each vendor defines and prices a credit differently, so the term means something different from one product to the next.

Why is credit-based pricing so hard to evaluate? Because a credit has no standard unit, no benchmark to forecast against, and varies in cost from one action to the next. 55% of buyers find credit and token pricing harder to evaluate for AI than traditional SaaS – more than any other model, and consistently across company sizes.

How much does an AI credit cost? It depends entirely on the vendor. A Salesforce Flex Credit is about $0.005; a Lovable credit is about $0.25 – roughly a 50x difference, with a different unit of work behind each. Comparing the per-credit price across vendors is misleading, because the work one credit buys isn't the same.

What makes a good credit pricing model? A consistent definition across teams, a credit that maps to one discrete action, allotments that scale fairly with usage, documented rollover and expiration rules, and – above all – a way for buyers to forecast their spend before they commit.

How should buyers evaluate a credit-based AI tool? Ignore the headline price per credit and focus on total expected spend: ask how many credits a typical task in your workflow consumes, what a comparable customer spent, and whether there's a calculator or estimate available before signing. If a vendor can't help you forecast the bill, treat that as the risk.

Ready to grow with confident pricing?

Let's start a conversation with our team that will deliver practical value even if you don't work with us.

.png)